Understanding Financials – Loan Application Process

Australia’s No 1 Assignment Help began its Online Assignment Help with the desire to serve students who are struggling in almost any subject with the support of our Professional Assignment Writers. Each of these academic writers possesses extensive knowledge and expertise. Students can avail our Assignment Writing Service at any time. We facilitate our services in whole Australia.

Section 2 – Loan characteristics

Learning outcomes

Upon completion of this section you will be able to:

- identify various types of mortgage loans and the similarities and differences between them

- understand and apply the generic loan fundamentals

- analyse the loan requirement of your client and apply this knowledge to the choice of mortgage loan product

- understand the working of loan serviceability

- understand the basics of negative gearing

- have knowledge of the peripheral products offered by lending

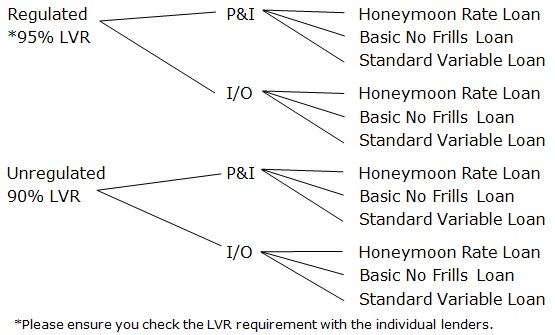

Core lending products

There are many different types of mortgage loans in the market. The lenders have different policies and guidelines for the individual products and they often vary from lender to lender. Finance/Mortgage Brokers will be constantly questioned on the terms and conditions of the various Bank products and it is extremely important for the broker to be up to date with product specifications.

Brokers should also be advised that the banks change their product specifications often. If you are using prescribed software from your aggregator or franchisee, or if you lease a system, the changes should be managed by the IT departments. However the lender will notify the broker by regular bulletins and it is extremely important that you allow time in your schedule to absorb the changes.

Many of the lenders also run up-date sessions or in conjunction with your aggregator or franchisee. It is important to attend as many as you can to keep yourself up to date with the changes. The BDM’s for the lenders also give you excellent assistance if you are in doubt as to a product specification and how to structure loans to give you the best chance of a successful submission. If in doubt, always check before submitting the loan.

The following are outlines of the three core products currently in the market.

Standard variable rate

As the name implies this product caters for the clients wanting a loan that has a variable interest rate. This means that the interest rate fluctuates with changing market conditions. As outlined previously, this is determined by the economic climate and is administered by the individual lenders. This product’s rate may move when the Reserve Bank of Australia (RBA) makes interest rate adjustments. Although this change in official cash rates may happen, any changes are at the lenders discretion. All other variable rate products may then be adjusted accordingly.

Standard variable rate home loans are the most common home loans in the market. There are slight variations to the basic standard variable home loan such as ‘honeymoon rate’ loans. These will be discussed further in this section.

When taking out a standard variable rate loan, the borrower takes on the risk that the rates may increase or to their benefit, may fall. Back in the 90’s interest rates soared to around 18% which forced many people to sell their properties as they could not afford the repayments.

Standard variable home loans can be either regulated or unregulated under the NCCP depending on the purpose of the loan. As we have learned in the earlier sections, if the loan funds are being used for the purchase of property predominantly for personal or domestic use or residential real estate investment and improvement, it is covered by the NCCP making it a loan. If a residential real estate property is being used a security to provide funding predominantly for business/investment purposes (residential real estate excluded), it is not covered under the NCCP and is deemed an unregulated loan. Let us have a look at the loan types available:

| Loan purpose | SVR loans can be used for personal or investment purposes. These may include:

• purchase residential owner/occupier property • purchase residential investment property • purchase vacant land • construct a residential home • purchase motor vehicle • purchase shares for personal investment • holiday • other personal requirements |

| Loan amounts | These are subject to the individual lender’s discretion, but usually the minimum amount would be $10,000 with no maximum amount The maximum is dependent on the borrower’s ability to repay and the LVR. |

| Term | Up to 30 years, more commonly 25 years. |

| Repayments | The repayments are usually calculated as principal and interest repayments and can be paid weekly, fortnightly or monthly. |

| Extra repayments | Usually allowed without penalty. |

| Early payout fees | There is usually no penalty for paying out a SVR loan. |

| Redraw facility | Generally available – some lenders will charge a fee. |

| Fees | Usual fees paid on a SVR contract may include:

• Loan establishment fee • Government required fees such as stamp duty (Depending on State), title search and registration of mortgage document • Valuation fees • Progress inspection fees (construction) • Ongoing loan maintenance fees. |

| Security | Registered first or second mortgage over a residential property. |

| LVR | Regulated – 95%

Unregulated – 90% |

| LMI requirements | Lender’s mortgage insurance is required for loans above 80% LVR. |

This information is general and the individual lender criteria should be consulted for each loan application.

Let us now have a look at the options available for the SVR loans.

Basic variable rate loan

As the name implies, this type of loan has most of the characteristics of the standard variable rate loan, but is offered by some lenders as a budget or economy style loan. The main feature of this loan type is the reduced interest rate. This loan is often referred to as a ‘no frills’ or basic loan. In some cases, there is no ongoing fee per month (please check with the individual lending institutions). There are fewer features than those applicable to the SVR products. There is usually no redraw facility.

| Loan purpose | Basic variable rate loans can be used for personal or investment purposes. These may include:

• purchase residential owner/occupier property • purchase residential investment property • purchase vacant land • construct a residential home • purchase motor vehicle • purchase shares for personal investment • holiday • other personal requirements |

| Loan amounts | These are subject to the individual lender’s discretion, but usually the minimum amount would be $10,000 with no maximum amount The maximum is dependent on the borrower’s ability to repay and the LVR. |

| Term | Up to 30 years, more commonly 25 years. |

| Repayments | The repayments are usually calculated as principal and interest repayments and can be paid weekly, fortnightly or monthly. |

| Extra repayments | Usually allowed without penalty. |

| Early payout fees | There is usually no penalty for paying out a Basic variable rate loan. |

| Redraw facility | Generally not available. |

| Fees | Usual fees paid on a Basic variable rate contract may include:

• Loan establishment fee • Government required fees such as stamp duty, (depending on State) title search and registration of mortgage document • Valuation fees • Progress inspection fees (construction) • Ongoing loan maintenance fees |

| Security | Registered first or second mortgage over a residential property. |

| LVR | Regulated – 95%

Unregulated – 90% |

| LMI requirements | Lender’s mortgage insurance is required for loans above 80% LVR. |

Introductory/honeymoon rate loan

Lenders often offer teaser rates to encourage borrowers to use their funds. These loans operate the same as the standard variable loans but they have a period in the beginning of the loan where the interest rate is lower than the standard rate. This is usually somewhere around 1% lower for a period usually no longer than 12 months.

One specific area to note is that some lenders will impose payout penalties if the loan is paid out within the first three years.

| Loan purpose | Introductory/Honeymoon rate loans can be used for personal or investment purposes. These may include:

• purchase residential owner/occupier property • purchase residential investment property • purchase vacant land • construct a residential home • purchase motor vehicle • purchase shares for personal investment • holiday • other personal requirements |

| Loan amounts | These are subject to the individual lender discretion, but usually the minimum amount would be $10,000 with no maximum amount The maximum is dependent on the borrower’s ability to repay and the LVR. |

| Term | Up to 30 years, more commonly 25 years. |

| Repayments | The repayments are usually calculated as principal and interest repayments and can be paid weekly, fortnightly or monthly. |

| Extra repayments | Usually allowed without penalty. |

| Early payout fees | Allowed, some lenders will charge a fee i.e. 30 days interest penalty based on the current SVR and original amount financed. A sliding scale bases, percentage of the loan amount. |

| Fees | Usual fees paid on an Introductory/Honeymoon rate loans contract may include:

• Loan establishment fee • Government required fees such as stamp duty, (depending on State) title search and registration of mortgage document • Valuation fees • Progress inspection fees (construction) • Ongoing loan maintenance fees. |

| Security | Registered first or second mortgage over a residential property. |

| LVR | Regulated – 95%

Unregulated – 90% |

| LMI requirements | Lender’s mortgage insurance is required for loans above 80% LVR. |

Fixed rate loan

As the name implies these loans have the interest rate fixed for a certain term and therefore the repayments remain constant. This loan is available for the borrower who wants certainty in their interest rate and repayments for a certain period of time, thus protecting themselves from any increase in rate. These loans can usually be fixed for somewhere between one and five years although there are products available for seven and 10 years.

At the end of this fixed period, the lender will renegotiate another fixed period at their discretion and at the current lending rates. If the borrower wishes, they can at this stage, convert the loan to a variable rate. Lenders have made some changes recently where clients can change and increase their payments, but not to exceed $5,000 – $10,000 in any one year (check individual Lenders’ policies).

| Loan purpose | Fixed rate loans can be used for personal or investment purposes. These may include:

• purchase residential owner/occupier property • purchase residential investment property • purchase vacant land • construct a residential home • purchase motor vehicle • purchase shares for personal investment • holiday • other personal requirements. |

| Loan amounts | These are subject to the individual lenders discretion, but usually the minimum amount would be $10,000 with no maximum amount The maximum is dependent on the borrower’s ability to repay and the LVR. |

| Term | Fixed period from one to five years. Longer periods are available from some lenders. Including this period, the total period of the loan can be written up to 30 years, more commonly 25 years. |

| Repayments | The repayments are usually calculated as principal and interest repayments and can be paid weekly, fortnightly or monthly. It is quite common to have interest only payments available in particular for investment borrowing. |

| Extra repayments | Some lenders will allow up to a specific amount of extra repayments per annum. |

| Redraw | Some lenders will allow but will charge a fee. |

| Early payout fees | There will usually be a fee charged for early termination of a fixed rate contract. |

| Fees | Usual fees paid on a fixed rate loan contract may include:

• Loan establishment fee • Government required fees such as stamp duty, (depending on State) title search and registration of mortgage document • Valuation fees • Progress inspection fees (construction) • Ongoing loan maintenance fees |

| Security | Registered first or second mortgage over a residential property. |

| LVR | Regulated – 95%

Unregulated – 90% |

| LMI requirements | Lender’s mortgage insurance is required for loans above 80% LVR. |

In many cases borrowers, because of interest rate fluctuations, choose to operate split facilities (part of the loan amount fixed rate and/or, part of the loan amount variable rate and/or part of the loan amount, line of credit) to reduce the impact should this type of situation occur with increased interest rates.

Some lenders offer a rate lock fee (usually around .15% of the loan amount or min $550, whichever one is higher). This enables the client to fix the rate no matter what the rate is at the time of settlement.

Generally, the rate lock is available for 90 days, meaning the loan needs to settle within the 90 days. Otherwise, the client will settle with whatever rate it is at the time of settlement.

Line of credit

This type of loan is basically an overdraft using the home as security.

A limit is set (this is determined by the value of the property and the ability for the borrower to repay) and the borrower may then deposit and withdraw from this account staying within the limit. The interest is calculated on the daily outstanding balance and is debited monthly to the account. The minimum repayment on the account must therefore be the interest charged.

The account is usually operated in a way that the borrower deposits wages (income) to the account and then uses a credit card (up to 55 days interest free) for the monthly purchases. One withdrawal is then made to pay off the credit card. This keeps the loan account balance as low as possible for the month, and therefore the interest that has been calculated throughout the month is on the reduced balance. The sequence then starts again for the following month.

| Loan purpose | Line of credit loans can be used for personal or investment purposes. These may include:

• purchase residential owner/occupier property • purchase residential investment property • purchase vacant land • construct a residential home • purchase motor vehicle • purchase shares for personal investment • holiday • other personal requirements. |

| Loan amounts | These are subject to the individual lender’s discretion, but usually the minimum amount would be $20,000 with no maximum amount. The maximum is dependent on the borrower’s ability to repay and the LVR. |

| Term | Evergreen or commonly 25 years. |

| Repayments | Repayments on a line of credit can be interest only or principal reductions. Payments can be made at any time. |

| Early payout fees | Normally no – check with lender. |

| Fees | Usual fees paid on a line of credit loan contract may include:

• Loan establishment fee • Government required fees such as stamp duty, (depending on State) title search and registration of mortgage document • Valuation fees • Ongoing loan maintenance fees – usually $8–$15 per month. Some lenders will charge annually or six monthly. |

| Security | Registered first or second mortgage over a residential property. |

| LVR | Regulated – 90%

Unregulated – 90% |

| LMI requirements | Lender’s mortgage insurance is required for loans above 80% LVR. |

Amortising line of credit

These loans operate in the same manner as an Equity Line of Credit with one main difference. The Equity Line of Credit requires a minimum monthly payment of interest only whereas the amortising Lines of Credit require a minimum monthly payment equalling that of principal and interest. This means that if the loan is written over a term of 25 years, then the calculated principal and interest repayments for this term would apply. The borrower may however pay in excess of this and redraw on the account only up to the limit now determined by these principal and Interest (P&I) repayments.

| Loan purpose | Line of credit loans can be used for personal or investment purposes. These may include:

• purchase residential owner/occupier property • purchase residential investment property • purchase vacant land • construct a residential home • purchase motor vehicle • purchase shares for personal investment • holiday • other personal requirements. |

| Loan amounts | These are subject to the individual lenders discretion, but usually the minimum amount would be $20,000 with no maximum amount. The maximum is dependent on the borrower’s ability to repay and the LVR. |

| Term | Up to 30 years, more commonly 25 years. |

| Repayments | Repayments on a line of credit can be interest only or principal and interest. Payments can be made at any time. |

| Early payout fees | Normally no – check with lender. |

| Fees | Usual fees paid on a line of credit loan contract may include:

• Loan establishment fee • Government required fees such as stamp duty, (depending on State) title search and registration of mortgage document • Valuation fees • Ongoing loan maintenance fees – usually $8 – $15 per month. Some lenders will charge annually or six monthly. |

| Security | Registered first or second mortgage over a residential property. |

| LVR | Regulated – 95%

Unregulated – 95% |

| LMI requirements | Lender’s mortgage insurance is required for loans above 80% LVR. |

Construction loans

Most lenders will finance properties under construction for owner occupied or investment purposes. Construction loans may be a little more complex than the standard residential purchase as they require funding progressively. The lender will make payments to the builder at various stages of construction.

Lenders will generally require borrowers to use any type of variable rate loan product until the construction has been completed. At this stage the borrower can switch to a fixed rate or line of credit type product. This may incur a switching fee. This should be checked prior to the application being lodged.

Clients usually purchase a block of land before entering into an agreement with a registered builder. To secure the block of land, you would make a loan application (Max LVR 90%) and go to settlement on the block of land. At the same time it is sensible to request a pre- approval for up to the total end value, (costs of Land and House together – max LVR 95%). Therefore, the clients secure the block of land and then they know they can go shopping for a builder.

Once the clients have found a house they wish to build, in addition to the normal loan application requirements, you must also supply the following:

- Registered Builders Certificate

- Fixed Price Building Contract

- Council Approved Plans and Specification

- Specifications and schedule of progress

You will need to forward copies of these to the lender and ask for unconditional approval. The bank will send these documents to the valuer to make an ‘on completion valuation’ and ensure the client is going to have built what has been agreed to in the contract.

The banks insist the client use their agreed own funds first, usually towards the purchase of the block of land. If the First Home Owners Grant (FHOG) is being used, this will go to the builder in the first progress claim. Usually there is four or five progress claims. Once the builder has completed a stage of construction, they will send an invoice to the lender and to the client. The client must inspect the construction and usually advises the lender by signing an authority to authorise the lender to pay the progress claim, drawn from the loan, to the builder.

The valuer would normally make two inspections—one at about mid construction stage and one on completion. The final progress payment is not usually made until after the final inspection. There are usually four progress payments made to the builder over the term of construction.

The general stages of payment may differ, dependent upon the state and may also be referred to differently as follows:

- Pad (slab) down or foundation stage

- Walls constructed – plate high, frame stage

- Roof

- Lock up stage

- On completion

- Remember that a deposit is usually included in the contract prior to commencement of the

During the construction period, the clients’ payments will be interest only, calculated on the current outstanding debt. When the loan is fully drawn their repayments of P&I will commence. If clients have chosen a Fixed Rate Loan, this rate and term will commence at the time of final draw down.

Below are two scenarios to assist with you understanding construction loans.

Facts to take into consideration:

- In both scenarios our borrowers are first home buyers and they are receiving the First Home Owners Grant

- They have genuine savings as deposits

- They have additional funds for miscellaneous costs

- They have a contract of sale and full plans and specifications from the

Scenario 1—Purchase a house and land package

| Value of land:

Price of house to construct Total Security |

$200,000

$180,000 $380,000 |

| Maximum LVR = 95%

Maximum loan amount |

$380,000 x 95%

$361,000 |

| Deposit required = 5% (genuine savings) | $380,000 x 5%

$ 19,000 |

In this scenario, the borrower would only need to submit one loan application to cover both the house and land purchase as a package. They would need to fund a deposit of $19,000 plus costs. (The funds for costs can come from a combination of savings, first home owners grant or gifts.)

Scenario 2—Purchase vacant land and begin construction within 12 months

| Value of land:

Total Security |

$200,000

$200,000 |

| Maximum LVR = 90%

Maximum loan amount |

$200,000 x 90%

$180,000 |

| Deposit required = 10% (genuine savings) | $200,000 x 10%

$ 20,000 |

| Within the 12 month period, the borrower must:

• Find a registered builder • Arrange plans, specifications and price of home • Sign a fixed price contract • Commence construction |

$180,000 |

| Value of:

• House • Land New total security |

$180,000 $200,000 $380,000 |

| LVR = 95% (house and land)

Maximum loan amount |

$380,000 x 95%

$361,000 |

In this scenario, the borrower would need to submit one loan application to cover the land principle purchase and would settle the land portion of the contract. They would be wise at the application stage to apply also for an approval in principle for the construction of the house. Although the exact amount is unknown, an approximate figure can be approved awaiting plans and specifications etc. The borrower would need to fund a deposit of $20,000 plus costs. (The funds for costs can come from a combination of savings, first home owners grant or gifts.) Once the construction is ready to commence, the land loan would be combined with the cost of the construction and one loan would emerge.

This scenario demonstrates an excellent way for clients to secure a block of land, especially when new land is released. This then gives them time to decide on a house to build.

You will notice the difference in Scenario 2 where to purchase the land first, then construct the house at a later date, clients will need to save or have in their account the 10% deposit for the block of land (plus costs), (5% of the value of the purchase price is still required to be genuine savings). In Scenario 1, they actually needed 5% (which must be genuine savings, $19,000) of the total land and house package deposit to be able to purchase the land and construct the house via one application.

Family pledge/equity

Family pledge allows borrowers to access finance for the full property purchase price, plus a further 10% of the costs involved. To enable this, an immediate family member provides a limited personal guarantee for the pledged amount, supported by equity in their existing property.

This type of loan is suited to first home buyers with no deposit, who have an immediate family member that is willing and able to offer security support. Its purpose is for purchase or construction of a residential owner occupied or investment property.

In an environment of increasing home prices and declining affordability, it is difficult for borrowers to save the required deposit to purchase a home. The family pledge product allows borrowers to own their own home sooner by allowing them to borrow the full purchase price plus an additional 10% to cover costs.

Popular loan features/packages

With many of the loan types that we have discussed previously, the lenders can offer certain features and benefits and also package the various loan types together. The following will give a general outline of some of those features and packages offered.

Split facilities

This is not a type of loan, but more the different combination of loans. Split facilities, as the name implies, allow borrowers to have a portion of their loan as one type of loan e.g. Standard variable, whilst the other portion can be another type e.g. Line of Credit.

The reasons for using this type of facility are many. Perhaps the client wants to fix a portion of their loan to safeguard themselves in the event of a rise in interest rates. They may wish to have the flexibility of a line of credit, but they do not want the temptation of retaining a high loan balance. They can therefore have a portion on line of credit and a portion on another product.

Using a split facility gives you the benefit of having two or more loan types with only one ongoing fee (with most lenders).

An example of a typical split could be for a $250,000 loan, the borrower may decide that they would like to have the convenience of having money at call and although they only need $220,000 to purchase their home, they borrow $200,000 at a Standard Variable rate and then have $50,000 on a line of credit. They could then use the $20,000 required from the line of credit and have $30,000 available for personal use.

This may include such things as holiday, home improvements, unexpected household or car repairs etc. The borrower would then have the major part of the loan at the lower standard variable rate and would only be paying interest on the line of credit for the outstanding amount not the credit limit.

Another popular split is that of having part of the loan standard variable and part fixed. We learnt in an earlier section that standard variable rates fluctuated with the economic environment but the fixed rates remained constant for the term of the fixed rate contract. This gives the borrower comfort in knowing that if rates rise it will only affect a portion of their loan.

These combinations of products are extremely popular and brokers should be very conversant with the various combinations available.

Mortgage offset

The Mortgage Offset account is an option available to certain types of loans. It can have the same effect as a line of credit whereby the balance of this account is offset against the loan balance thus saving interest. This is often attractive for the borrower who still wishes to operate a savings account to know how much money that they really have saved. It works simply by linking a standard variable loan to a standard cheque/savings account.

This means that if a borrower has a loan balance of $100,000 and a savings account balance in a 100% offset account of $10,000 the borrower will only be charged interest on $90,000 being the difference between the two accounts. Some lenders will only allow part of the savings balance to be offset against the loan balance. This type of loan can work as effectively as Lines of Credit without the borrower feeling that they have no money in the bank. Loan repayments must be made on the full approved loan amount.

These offset accounts can be used for both owner occupier loans as well as investment loans and can be tax effective in the way that the interest that the borrower would normally earn on the savings account would be classed as income and taxed accordingly. In this instance, there is no interest earned on the offset account.

Note: Post March 2004, this product will be deemed a ‘deposit product’ and as such will be captured under legislation applicable to ASIC Public Statement 146 (PS 146). In essence this means you cannot give advice on this product unless you are licensed under the applicable code.

Professional packages

These are usually packages put together by individual lenders to cater for specific high net worth clients. They include combinations of loan types, loan peripherals such as credit cards and accounts at favourable rates and offers of other bank services. Eligible applicants may be categorised by profession, income levels, and increasingly the level of borrowings.

The products used are normally a combination standard variable/ honeymoon rate products, mortgage offset or line of credit. The combined total of the loan package decides the discounts applicable.

These products are generally discounted by around 0.5%–1% and usually have discounted or nil ongoing fees. A compulsory favourable Credit Card may also form part of this package. Other features include fee free banking and access to Financial Planners and Private Banking on favourable conditions for an annual fee.

These packages vary from lender to lender.

Interest only

This is used mainly for investment purpose lending, e.g. purchasing a rental property. The borrower may wish to pay interest only as this is more advantageous for tax deductibility. This is normally available for most loan types, standard variable, fixed rate loans and Equity Lines of Credit.

Interest in advance

This is also used for investment lending purposes where a borrower may wish to pay up to 12 months interest in advance for the following tax year to enable them to claim the interest in the current tax year. These payments can only be made in June each year, for the following tax year and claimable in year of payment. The rate is fixed for the next twelve month period and is usually a discounted rate.

Bridging finance

This is short-term finance provided usually when a client is transferring from one home to another and the new home is settling prior to the settlement of the current home. The contract is usually written as a standard variable loan and is reviewed after 12 months. The repayments are usually interest only and in some cases are capitalised (added to the loan balance). Calculating the loan amount and interest component of these loans is quite different to standard loans and brokers are advised to check thoroughly each lenders calculation method before writing these loans. Commission is paid on the End Debt of the bridging loan after the original property is settled and the bridging component of the loan is finalised.

Lo-doc/No-doc loans

This is the term to describe loan facilities where the lending institutions require minimal or no documentation to verify income for loan applicants, who are self-employed. There are usually LVR limitations on these loans but the main issue is that in most cases the client self-certifies their income levels or the level of loan repayment they believe they can afford for the loan they wish to borrow. In most cases they sign a statement (or obtain one from their accountant) that they earn a certain level of income or that they can maintain repayments at a certain level and supply BAS statements to support their loan application.

The reason for these types of loans can be many and varied, such as the client’s financials may not be prepared yet, or they may have only been in business for a short period of time so there are no financials available. The lenders are taking a commercial risk that the clients understand their commitment and will meet their repayments. They mitigate the risks by limiting the LVR or relying on the client’s previous good repayment history and the value of the security property. In the case of non-conforming lenders they also usually charge a higher interest rate to mitigate risk.

Parenting Repayment Break (PRB)

Borrowers who are on/or planning to take maternity/paternity leave will have the ability to take a brief break in repayments.

| Feature | Product Parameters (Summary) |

| Max LVR | · 90% – at time of request. |

| Loan Purpose | · Owner-occupied loans only. |

| Credit History | · Minimum of 12 months of satisfactory loan repayment prior to allowing a Parenting Repayment Break

· Repayment history must be clear of missed/late payments for at least 6 months. |

| Repayment Type | · Interest only is not permitted. |

| Other | · Parenting Repayment Break may be taken as either:

o 3 months ‘no repayments’ or o 6 months ‘half repayments’. · Maximum of 2 Parenting Repayment Breaks during life of loan · 12 full monthly payments must be made between each subsequent Parenting Repayment Break · Repayments to be re-amortised over remaining term following a Parenting Repayment Break. |

| Documentation | · Lender is to retain evidence of:

o Evidence of maternity/paternity leave approval o Lenders approval of Parenting Repayment Break o Re-amortisation, serviceability calculations and o Income evidence (if applicable). |

Other loan features

Redraw facilities

Some loan types allow you to pay extra funds into the loan to reduce the loan balance and then should the need arise; you are able to redraw the extra funds that you have paid. The lender may stipulate a minimum amount able to be redrawn and charge a fee for the service.

Fee-free savings/cheque accounts

Some loan packages offer a fee free transactional account (savings/cheque) allowing unlimited deposits and withdrawals. The terms and conditions of these accounts should be checked with each lender. Some lenders also offer fee free credit cards. Interest is still charged after the interest free period of the account, but there are no other account keeping fees, etc.

Fees

With all loan types there are going to be fees attached. The following are some of the fees that you will need to explain to your borrower. Actual fees and calculations will be discussed in Section 9.

Ongoing fees

These fees are charged on a monthly basis i.e. added to the loan balance. These fees are around $8.00–$12.00 per month. It is advisable to take this into consideration when comparing product costs over a particular term of the loan. These fees can change throughout the life of the loan. Some bank products opt for a once a year fee which at first seem expensive but they are often offset by other features such as no transaction fees or lower rates.

These are mainly evident in Professional packages.

Establishment fees

These one off fees are charged at the inception of the loan. Some lenders will discount or waive the establishment fee to entice potential customers.

Valuation fees

This is a one off fee that is often included in the lender’s establishment fee. If more than one property is required to be valued, a further fee is usually required. Each lender’s fee may differ and therefore must be verified. An indicative figure would be $250–$300.

Property purchase stamp duty

This is a one off fee paid to the government and depending on the state that the transaction is in, can be calculated on the purchase price or the market value of the property, whichever is greater.

Mortgage stamp duty

This is a one off government fee charged as a percentage of the loan amount. (Depending on which State)

Solicitor/settlement agent fee

This is a fee charged by the solicitor or settlement agent to prepare documents, attend and finalise settlement on your behalf. The fees can vary significantly from agent to agent and state to state.

Registration of mortgage fee

This is a fee to register the mortgage with the land titles office.

Discharge of mortgage fee

This is a one off payment required to register the discharge of mortgage to the land titles office.

Register of transfer of title

This is a one off payment required to be paid to register the transfer of ownership to the land titles office.

Title search

This is a one off payment required to be paid for the search of title to the land titles office.

Bank peripherals and our obligations

In this section you will learn of the other types of bank products available and our obligation to advise the clients of their availability. Bank peripherals refer to the bank products other than loans, about which a broker may not have informed the client. While there is generally no obligation for the broker to sell these other products it is very much in their interest to do so.

- Knowledge of the peripheral products increases the credibility of the broker and enhances the sale of the loan For example with the popularity and availability of professional packages there is an expectation that these products go with the package.

- If the broker does not involve himself/herself with the peripheral products the bank certainly will and this can give the client the impression that the broker either did not know, or care about selling the The broker, must at all times maximise the experience for the client to ensure an ongoing relationship and advising them of the very favourable products that may go with their package will enhance that relationship.

- The more products a client has with a bank the more reluctant a client is to move elsewhere. It is always wise to market all the products you can while you are involved to ensure the client will stay with you in the The time the clients are writing the loan is the prime time to establish all the other products and ‘bed’ them down with a total range of products.

This highlights your expertise and your interest in giving them a total package. This in turn encourages the client to remain loyal to the person who solved all their finance issues, not just their loan.

The broker should always be concerned with putting a protective screen around their clients and the number of products makes it possible to achieve these goals. This in turn, builds a great professional relationship with your client, therefore they are less likely to contact the Lender directly and have you as the first point of reference.

Credit cards

Most banks offer credit cards as a part of their total lending packages. There are a number of home loan products that will include fee free credit cards in the package. Most credit cards will have an interest free period for up to 40 or 55 days.

The calculation of these interest free periods begins from the first day of the billing cycle. For instance, if a billing cycle on the credit card begins on the seventh day of the month, then anything purchased on that card on that day will give clients the full benefit of the interest free period.

The cycle will then continue through to the 6th day of the next month. At this stage a statement will be issued giving them (X) amount of days to pay the account before incurring interest.

With a forty day interest free period, then the account is likely to be due for payment nine days after the end of the monthly cycle, hence giving them the 31 days of the month plus nine days (total 40) to pay the account. The usual operation of a credit card is that the interest free period is applicable to purchases not to cash advances. Cash advances incur interest charges immediately.

We should be able to advise our clients of the operation of the credit cards attached to their lending facilities. In addition to this, we should know if they have interest free periods available. It is also very important for us to know what interest rate the client will be charged if they do not clear their credit card balance in the required time or make cash withdrawals. Some banks will only offer ‘debit cards’. These cards will still be able to be operated through the credit card networks, such as Visa. The cards will have this branding stamped on them. The difference is that there is no overdraft amount. The client can only draw upon the funds that they have in their account. If a credit card does not come in the total loan package, it is likely that the bank will charge an annual fee.

This will differ between banks and this fee should be advised to your client during the course of your presentation.

Cheque/savings accounts

As with the credit cards facility, a number of lenders will offer a fee free cheque/savings account into the loan package. The individual banks will have their own schedule of fees for each of the accounts. As an added service to your clients, it is advisable to have brochures of fees and charges for them. The clients would also be able to get this information from the help lines, so have a list of these numbers available.

Other lending departments

Other lending areas such as personal loans, business loans and commercial loans are also part of the bank’s portfolio of products. These areas are used by a number of Finance/Mortgage Brokers as additional products for their clients. You would need to discuss the availability of these products with your own company managers.

Term deposits

This type of account is for investors and is not something that we need to discuss with our clients. This investment account allows clients to deposit amounts of money into the bank at a higher interest rate than the normal saving accounts as they are agreeing to have their money invested for a certain period of time. These rates change regularly but once the client is locked into a specific term, the interest rate would remain constant for that period of time.

Risk management products

General insurance

A number of banks offer general insurance products (i.e. home and contents, motor vehicle, personal valuable insurance etc.). You are obliged to advise your client that they will be required to obtain insurance to protect their home. This will be required prior to settlement of the loan and a certificate of currency will be required noting the bank’s interest in the property. You are able to advise them that the bank offers this service or whoever you may have an arrangement with, but you cannot force them to use either source. They must be free to make their own choice but with the knowledge that this insurance is a requirement.

Financial planning

This service is generally offered by most banks and in particular with some, is a major area of the bank. Again, you are able to advise your clients that the bank or whoever you have an arrangement with, offer this service and suggest that it would be in their best interest to discuss their needs in this area with these financial planners. However you cannot force them to follow your suggestion.

It is our experience that client loyalty is best served by referring them to a Financial Planner or Insurance Broker with whom you have reciprocal, loyal relationship and you can vouch for the professional ethical standards they exhibit. If the clients choose to accept advice from a bank employed financial planner the planners may understandably be more inclined to direct the clients to bank lenders for future transactions, in spite of your good service.

It is the usual practice of a number of banks to do follow up calls with their clients in order to assist them with Financial Planning or Insurance. If you have already passed their details onto an external Financial Planner or Insurance Broker it would be advisable to let your client know that the bank is likely to contact them anyway.

Life insurance

Term life insurance

This is the simplest form of life insurance. It gives your dependents a lump sum when you die. Like house or car insurance a premium is paid each year for annual protection.

The policy has no savings value and unless the premium is paid each year there is no further cover, and the policy will lapse.

The amount of insurance required will vary for each household depending on the size of mortgage, other debts, provisions for children and future income needs.

Having decided the amount of insurance required it is necessary to check whether life insurance is provided as a part of your superannuation fund. For example only, experts may recommend life cover of about 10-15 times pre-tax income is required for both income earners.

If there have been no nominated beneficiaries, the insurer will pay the agreed insured amount to your estate.

Total and permanent disablement insurance

In addition to Life Insurance you may also apply for Total Permanent Disablement (TPD) insurance. This optional benefit is available for an additional premium. If you obtain TPD Insurance in the event of you becoming totally and permanently disabled, the Insurer will pay you the agreed insured amount as a lump sum. It depends on whether you take cover for you own occupation or any occupation and what the insurer considers relevant to their policy when assessing a claim.

Income protection insurance

This gives you financial protection if you are disabled through injury or sickness and are unable to work. If this happens, the insurance company pays you a portion of your monthly income, normally 75% of your annual gross income, which is calculated to a monthly amount.

Cover can be taken out for certain waiting periods of 14, 30, 60; 90 days and cover can range from two years to age 65 years. Naturally the longer the term of cover and the shorter the waiting period the higher the premium costs. Your occupation and smoking or non-smoking habits along with any other known illnesses are taken into account when assessing your application and the premium. This type of cover is also sometimes referred to as Salary Continuance Insurance.

Taxation benefits are available for this type of cover and you should consult your accountant in regards to these.

Business expenses insurance

If you are self-employed, this insurance covers the business expenses that you must pay each month even if you are unable to work because of illness or injury.

Trauma insurance

In addition to Life or Life and TPD insurance you may apply for Trauma insurance. The optional benefit is available for an additional premium. This benefit eases the financial burden of the costs associated with recovering from a medical crisis. The insurer will provide a lump sum payment to you if you are diagnosed with a range of listed trauma events under their policy.

One must remember due to medical advancements these days most people survive the traumas and the average age for claims for this policy is between 45-55 years old.

Mortgage protection insurance

Mortgage Protection Insurance is specifically designed to protect the borrower against death, disability and involuntary unemployment. Cover varies quite markedly between providers of this type of insurance protection. However, usually on death the payout is limited to the outstanding amount of the loan at the time of death. (Some companies have level cover and will pay any extra amount over the debt owing to the client’s estate, e.g. initial mortgage of $250,000; MPI cover provided at $250,000; current mortgage debt at $200,000. The debt is fully repaid and the extra $50,000 is paid to the client’s estate.)

Disability benefit is limited to the mortgage repayments up to a maximum figure of approximately $4000 per month (varies between companies) and covers loan repayments for a limited time of around 2½ years (varies between companies).

Involuntary unemployment cover meets loan repayments for up to three months.

Lenders may make insurance cover a condition of the loan. What they cannot do is force the borrower to take out their insurance product. As such they cannot make MPI mandatory but can insist that the borrower obtain cover prior to releasing the funds.

MPI is generally more expensive yet does not provide the full protection that standard life insurance covers, such as Death, Permanent Disability and Trauma cover, and Income Protection.

Duty of Care

Under the Duty of Care a broker has a legal obligation to advise clients of the availability of the risk management products to protect themselves against unforeseen events as described above. The courts in Australia deem a broker to be a professional. By not raising the need for financial protection, a broker can be judged negligent under the Duty of Care.

Gearing

In this section, you will have a very basic look at gearing and when it is used. Brokers without the proper qualifications are not allowed to give any advice to their borrowers about gearing. It is pertinent to advise your client of this and suggest that he seek advice from their accountant or suitably qualified professional.

There are three types of gearing:

- Negative

- Neutral

- Positive

Negative gearing is an accounting term used when an asset is purchased for investment purposes and is returning an annual loss. This annual loss amount is then offset against annual income with the result of decreased tax assessments.

Neutral gearing applies when the annual cost of investment is equal to the annual income generated.

Positive gearing applies when the annual income generated is greater than the costs and returns an annual profit for the investor.

A common form of gearing is a client purchasing a rental property. The customer will usually borrow the maximum amount possible. The interest paid on this loan transaction along with other fees such as management fees (approximately 7% – 8% of rental income), maintenance costs, depreciation and other costs are then offset against the rental income. When there is a shortfall in the income received compared with the expenses incurred negative gearing results. This loss amount is then carried forward to the client’s income to decrease the amount of their taxable income.

For example, our client has purchased a property for $300,000 and has borrowed $225,000.

| Purchase price of property Amount of loan | $300,000

$225,000 |

|

| Income: | ||

| PAYG income | $80,000 | |

| Rental income @ $250pw | $13,000 | |

| Total income | $93,000 | |

| Rental property expenses: | ||

| Management fee @ 8½% | $ 1,105 | |

| Interest (calculated @ 7% interest only) | $15,750 | |

| Depreciation | $ 7,000 | |

| Land and water rates | $ 2,000 | |

| Maintenance | $ 1,500 | |

| Total expenses | $27,355 | |

| Taxable income | $65,645 | |

| Without rental property

Tax payable on total income of $80,000 = $23,136 Net income = $56,864 |

||

| With rental property

Total income = $93,000 – $27,355 (expenses) = $65,645 Tax payable on total income of $65,645 = $16,896 Net income = $48,749 |

||

The outcome from this scenario is that without the rental property, the client would be earning $80,000 and would pay $23,136 in tax. This would give him a net income of $56,864.

With purchasing the property the client would have a gross income of $65,645; he would pay $15,750 in repayments, $1,105 in management fees and $1,500 in maintenance costs and $2,000 in land and water rates. He would pay $16,896 in tax. Net income would therefore be $48,749.

This example shows that through negative gearing our client is able to purchase an investment property with the net difference to cash in his pocket being approximately $156.00 per week.

This is a very basic example and is used only for the purpose of demonstration. You must advise your client that they should seek their accountant’s advice prior to making any decisions on Negative Gearing.

An important reminder: Finance/Mortgage Brokers are not permitted to advise clients on negative gearing issues unless they have the necessary qualifications to do so. These qualifications are those requirements specified by the Australian Securities and Investments Commission (ASIC) as per ASIC Regulatory Guide 146 (RG146).

Other considerations would need to be made in respect to Capital Gains tax.