If you want help on FMA101 Financial Management TOPIC 3 – Cash Flow and Financial Planning Assignment Homework then please contact Assignmenthelpaus. We provide our service on various kinds of assignment work like Dissertation Writing Help, Case Study Assignment Help and MBA Assignment Help. We guarantee 100% plagiarism free work with the help of our 100+ expert writers.

TOPIC 3 Cash Flow and Financial Planning Assignment Answers

LEARNING OUTCOMES

After completing this topic, you should be able to:

- Explain the purpose, function and content of a statement of cash flows and calculate and analyse the operating cash flow and free cash flow of a business entity by using a variety of cash flow analysis techniques.

- Distinguish between including long-term (strategic) financial plans and short- term (operating) financial plans.

- Explain the purpose of a cash budget in the cash flow and financial planning process, and prepare and interpret the contents of a cash budget.

- Explain the purpose of pro-forma statements in financial planning and prepare and interpret a pro-forma statement of comprehensive income using the percent-of-sales method and interpret a pro-forma statement of financial position using the judgemental method.

READING

Before continuing with this topic, please read the following:

- Gitman et al. (2015: Chapter 4)

Please make sure that you also read this study guide carefully as it contains additional information that is not in the prescribed textbook.

INTRODUCTION

The key concepts that you must focus on are:

- the objective of cash flow analysis

- the purpose of a statement of cash flows

- the meaning of cash and cash equivalents

- the sources of cash inflows and the causes of cash outflows

- cash flows from operating activities, investment activities and financing activities, including depreciation, amortisation and depletion

- calculating, interpreting and explaining operating cash flow

- calculating, interpreting and explaining free cash flow

The entire content of this chapter is extremely important. Study it thoroughly.

Cash flow is the lifeblood of any business organisation. It is the main determinant of whether a business remains in operation and can continue to exist or run out of cash, become bankrupt and have to stop operating and close its doors.

You need to make sure that you can explain the objective of cash flow analysis as well as the purpose of a statement of cash flows.

You need to be able to distinguish between cash and cash equivalents, and also identify types of “cash equivalents” that form part of the cash flow of a business entity.

It is very important that you can distinguish between activities in an organisation that result in cash flowing into the organisation and activities that cause cash to flow out of the organisation.

You need to understand why, in a cash flow analysis, the activities of a business entity are classified into the three categories of operating activities, investment activities and financing activities, as well as the cash inflows and outflows associated with each of these groups of activities.

It is expected of you to be able to explain the effect that the cash inflows and outflows from each of these groups of activities have on the liquidity and solvency of a business entity.

The following article briefly describes the importance of cash flow and financial planning for a business entity and how to deal with the issues with respect to cash flow planning:

In any business, cash flow is the name of the game. Nothing will put a business under more surely than failure to manage its cash well. This is something that every small business struggles with.

A bank balance of $10,000 may feel quite comfortable to the entrepreneur – until he suddenly realises that he has $15,000 of bills to pay from it. To avoid such surprises, entrepreneurs quickly learn to do cash flow projections – tabulations of expected revenues and expenses for the next few weeks or months. Such projections are effective – to the extent that they are kept current and accurate.

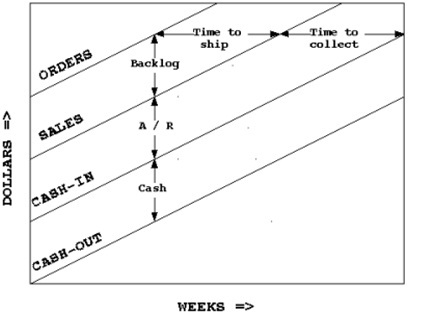

However, there is another tool to monitor and control cash flow, especially useful to manufacturing companies, that companies may wish to consider – the Cash Flow Graph.

This is a running plot of cumulative “orders”, “sales”, “cash in” and “cash out”. Its beauty for cash flow planning is the fact that what happens to your “orders” will be reflected in your “cash in”, i.e. time-to-ship plus time-to-collect are considered. If those times are running, say, 6 weeks each, this gives you a running 12 weeks’ advance knowledge of your “cash in” – plenty of time to do what you need to do to avoid cash problems.

Construction

The Cash Flow Graph is constructed as follows:

- Starting “cash out” = 0

- Starting “cash in” = Starting “cash out” plus Current cash balance

- Starting “sales” = Starting “cash in” plus Current accounts receivable

- Starting “orders” = Starting “sales” plus Current backlog and updated weekly as

- Cum “sales” at week(n) = Cum “sales” at week(n – 1) plus Sales week(n)

- Cum “orders” at week(n) = Cum “sales” at week(n) plus Current backlog

- Cum “cash in” at week(n) = Cum “sales” at week(n) minus Current accounts receivable

- Cum “cash out” at week(n) = Cum “cash in” at week(n) minus Current cash balance where

- Sales week(n) is what you have shipped and invoiced during week(n).

- The current backlog is what open orders you have to ship. (I included in backlog only that for which I had signed, hard-copy purchase orders in hand (i.e. POs I was willing to build against). However, other definitions are equally applicable – so long as they are consistently )

- Current accounts receivable is your total of all open (i.e. unpaid) customer invoices.

- Current cash balance is your total liquid cash (i.e. cash in the bank and/or money market).

I maintained these graphs on 11″ × 17″ graph paper (17″ vertical) over my desk for many years – and they proved invaluable.

Planning

The example graph shows a (impossibly) stable business. The “order”, “sales”, “cash in” and “cash out” rates are constant week after week. However, it does not appear to be a very healthy business since its “cash out” and “cash in” rates are equal. What we should be seeing is the “cash in” and “cash out” lines diverging as cash builds up (at a net-profit-before-tax rate). (Of course, this appearance of unprofitability may simply be because the owner is taking out all the “excess” cash.)

Time-to-ship is a measure of the resources (labour, materials, outside services, etc.) that you are putting into building and shipping product – and your efficiency in doing so. Time-to-collect is likewise a measure of your collection efforts.

Now let us assume that the “orders” line starts accelerating (i.e. curving upward). Time-to-ship will start to lengthen, i.e. the “sales” line will tend to continue along its present slope – unless you apply more resources to accelerate shipping. Of course, if you do, these added resources will have to be paid for – your payables- time (4 weeks?).

If you believe your accelerating orders will continue (i.e. that they are not just a temporary blip), test whether or not you can “afford” them. To do so, (lightly) project out your “cash out” line with those payments added. Then (lightly) project out your “sales” line (recognising that there may be some delay between the adding of resources and the consequent acceleration of sales). Then (lightly) project out your “cash in” line, a time-to-collect later than your projected “sales” line.

Now look at your projected cash balance. If it looks good to you, go ahead and add the needed resources – it looks like you can pay for them out of cash flow.

If your projected cash balance does not look that good, then you either need to raise some cash (debt or equity) to fund the growth – or accept the consequences of lengthening your time-to-ship.

There is no “right” or “wrong” to this decision. If you can raise the cash at an acceptable cost, do so. (Note: If you have receivables financing, do not overlook the fact that your projected receivables balance has increased.)

If you cannot raise the cash at an acceptable cost, then your lengthening time-to- ship will automatically reduce the slope of your “orders” line (through order cancellation) to what you can afford to ship. However, if this is the case, you better not let that reduction happen automatically.

Instead, take the initiative. Recognize that some customers are more profitable than others. Rather than waiting for customers to cancel randomly, cancel the least profitable yourself – so that you can more adequately service your more profitable. That is called “skimming the cream” – and is not at all an unreasonable response to cash and investment problems.

In any event, the Cash Flow Graph lets you make these kinds of decisions – with the best available data in front of you – long before they become cash crises. Of course, you still have to make timely decisions. If you defer the decisions, cash crises will result – but at least you will have had plenty of advance warning.

ANALYSING THE CASH FLOW OF A BUSINESS ENTITY

The key concepts that you must focus on are:

- making adjustments to cash flows to incorporate non-cash charges

- calculating and interpreting operating cash flow

- calculating and interpreting free cash flow

THE EFFECT OF NON-CASH CHARGES ON CASH FLOWS

Non-cash charges include depreciation, amortisation and depletion.

You should pay attention to how depreciation and other non-cash charges (amortisation and depletion) are treated in a cash flow analysis.

Depreciation is an accounting method of allocating the cost of a tangible asset over its useful life or life expectancy. Companies are permitted to deduct depreciation as an “expense” for tax purposes. This reduces taxable income and consequently reduces the amount of tax that has to be paid (a cash outflow).

The South African Income Tax Act refers to depreciation allowances as “capital allowances and recoupments” and in everyday jargon as “wear-and-tear” allowances.

The depreciation amount does not represent an actual cash outflow and therefore the depreciation amount must be added back to the cash flow when doing a cash flow analysis.

Amortisation and depletion costs are treated in exactly the same way as depreciation in a cash flow analysis. The costs are also added back into the cash flows for analysis purposes.

Amortisation is an accounting method of allocating the cost of an intangible asset over its useful life.

Depletion is an accounting method used to allocate the cost of extracting natural resources such as timber, minerals and oil from the earth.

OPERATING CASH FLOW

Students generally find the calculation of operating cash flow and free cash flow challenging for the following reasons:

- They did not study the content of financial statements as explained and illustrated in chapter 3 thoroughly to make sure that they know what each element in each of these statements means and represents.

- Their lack of understanding of the content of financial statements results in them being unable to identify and select the correct information from the different financial statements in order to calculate the cash flows.

When calculating the operating cash flow for a business entity, you need to identify and extract three amounts from a statement of comprehensive income. These amounts are:

- The operating profit of the This is also referred to as the “Earnings Before Interest and Tax” (EBIT).

- The after-tax rate. This is indicated as (1 – Tax rate). If the tax rate, for example, is 30%, then the after-tax rate is (1 – 0.3) = 0.7 or 70%.

- The depreciation amount.

Example 4.1 in the prescribed textbook demonstrates and explains the calculation of operating cash flow. Study this example and make sure that you understand where the information to do the calculations was taken from as well as how the actual calculations were done.

FREE CASH FLOW

When calculating free cash flow, you need to do the following:

- Identify and extract the amount for depreciation from the most recent statement of comprehensive income.

- Identify and extract the amounts for non-current assets, current assets, trade and other receivables, and accruals from the statements of financial position for two consecutive periods.

- Calculate the changes that occurred in the items from the statements of financial position during the two consecutive periods.

Examples 4.2 and 4.3 in the prescribed textbook demonstrate and explain the calculation of operating cash flow. Study this example and make sure that you understand where the information to do the calculations was taken from as well as how the actual calculations were done.

THE FINANCIAL PLANNING PROCESS

The key concepts that you must focus on are:

- long-term financial plans

- short-term financial plans

- the information needed to prepare these plans

You should be able to explain the objective and importance of financial planning for an organisation.

You must be able to distinguish between long-term financial plans and short- term financial plans and the information needed in order to prepare these plans.

You should, however, bear in mind that not all organisations are as sophisticated in their planning processes as those referred to in the textbook. Many organisations do not spend nearly enough time planning their future business activities and preparing long-term and short-term financial plans as mentioned.

Financial plans are referred to as “budgets” and the preparation of these plans are referred to as “budgeting”.

CASH PLANNING – CASH BUDGETS

The key concepts that you must focus on are:

- the sales forecast

- cash receipts (cash sales and credit sales)

- cash disbursements (cash purchases and credit purchases)

- net cash flow

- required financing

- excess cash balances

The cash budget is one of the most important financial plans of any organisation because a lack of available cash at any point in time can have serious consequences for any business. Available cash represents the liquidity position of an organisation and affects the organisation’s ability to meet its obligations and secure its continuous existence.

You, therefore, must ensure that you have a very good in-depth knowledge of the value, purpose and preparation of cash budgets.

You need to study the general format of a cash budget as illustrated in Table 4.6 of the prescribed textbook. You will be expected to use this format should you be required to prepare a cash budget.

THE SALES FORECAST

The preparation of a cash budget starts with a sales forecast. The sales forecast can be the result of an external forecast, an internal forecast or a combination of these.

You need to realise that although organisations will endeavour to prepare the most realistic sales forecasts with the information they have at their disposal, these forecasts are not cast in concrete and changes both in the external environment and from within the organisation itself can have significant effects on the cash budget as the future turns into the present.

Organisations, therefore, generally continuously update their forecasts and cash budgets as circumstances change and the future materialises. A cash budget is therefore not a static one-off event. It is a continuous process.

From the learning material, you should realise that the forecasting of both cash receipts and disbursements, and the seriousness and effort that go into such forecasts will have a significant influence on the usefulness and accuracy of cash budgets.

The poorer the efforts to estimate expected cash receipts and disbursements, the bigger the chances of inaccurate cash budgets and nasty surprises as the planning period materialises.

You must be able to describe and discuss the procedure followed to prepare a cash budget, and identify the different elements that form part of a cash budget, their importance and contributions. Furthermore, you must be able to prepare a cash budget from the information provided.

CASH RECEIPTS

Cash receipts refer to all the anticipated income that a business expects to receive from its day-to-day operations and any other ad-hoc activities that may also produce income.

For cash budgeting purposes, cash receipts are divided into cash receipts, credit receipts and other income. These receipts are all cash inflows.

Care must be taken to ensure that all possible sources of cash inflows are identified and evaluated when preparing the cash receipts part of a cash budget. The cash budget must reflect all realistically anticipated cash receipts, irrespective of their source.

Credit receipts refer to the sales made to those customers who were granted credit facilities by the organisation. They buy and take possession of goods on the date of purchase but they have to pay for such purchases only at a later date. Credit terms generally range between 30 and 90 days.

Students generally find it challenging to understand how to calculate credit receipts and particularly how to allocate credit receipts to the correct time periods.

You need to study Example 4.5 and Table 4.7 thoroughly to make sure that you understand how credit receipts received at different time periods are allocated in a cash budget.

Because credit payments are received long after the dates of the actual purchases, these delayed receipts are referred to as lagged receipts.

CASH DISBURSEMENTS

Cash disbursements refer to the expenses that a business incurs during its day- to-day operations. Cash disbursements are all cash outflows.

Care must be taken to ensure that all possible sources of cash outflows are identified and evaluated when preparing the cash disbursement part of a cash budget. The cash budget must reflect all realistically anticipated cash outflows, irrespective of their source.

A distinction is made in the cash budget between payments made for purchases that directly relate to the sale of products or services and other expenses incurred to support the sales and general functioning of the organisation.

Purchases are split into cash purchases and credit purchases. Credit purchases from an organisation’s suppliers are those purchases for which the organisation is permitted to pay only at a much later date. The concept is the same as that of granting credit to customers, only in this instance the business is the customer.

Because payments for credit purchases are made long after the dates of the actual purchases, these delayed payments are referred to as lagged payments.

You need to study Example 4.6 and Table 4.8 thoroughly to make sure that you understand how credit purchases made at different time periods are allocated in a cash budget.

NET CASH

Net cash = Total cash receipts – Total cash disbursements

- The net cash amount will be a positive amount if total cash receipts > total cash

- The net cash amount will be a negative amount if total cash receipts < total cash

Study Table 4.9 to understand how net cash is calculated.

BEGINNING CASH AND ENDING CASH

The beginning cash refers to the amount of cash that a business has available at the end of one period and, therefore, available at the start of the following period. The period could be a day, a week, a month or any other period the business chooses for such purposes.

Having calculated the net cash for a period, the business will add the beginning cash to the net cash amount (whether it is positive or negative) in order to calculate the “ending cash” for the period.

It should be clear to you that the ending cash for period A will be the beginning cash for period B.

Study Table 4.9 to understand how ending cash is calculated.

MINIMUM CASH BALANCES

Some organisations prefer to have a minimum amount of cash available at all times and hence need to manage their cash inflows and outflows in such a way that the minimum cash balance required is maintained.

EXCESS CASH BALANCES (SURPLUS CASH)

Should the ending cash for a period exceed the minimum cash balance required, then it means that the business has more cash available than it needs at the time. This is known as excess cash balance.

Excess cash balance = Ending cash – Minimum cash balance

The business can invest the surplus cash in short-term marketable securities while the excess cash is not needed and earn additional interest (cash inflows) from these investments.

Study Table 4.9 to understand how excess balances (surplus cash) are calculated.

REQUIRED FINANCING

In the event that the ending cash for a period is less than the minimum balance required for the same period, it means that the business has a cash shortfall. It does not have enough cash to meet the cash required for its obligations for a specific period.

The business, therefore, needs to find additional cash to cover this shortage. The cash shortage is known as the required financing.

The business can finance this cash shortfall in one of the following ways:

- Selling any short-term marketable securities it owns

- Making use of short-term financing options to borrow the funds required

- Using both (a) and (b)

Study Table 4.9 to understand how required financing amounts (cash Shortfalls) are calculated.

PROFIT PLANNING: PRO-FORMA STATEMENTS

The key concepts that you must focus on are:

- pro-forma statements

- pro-forma statement of comprehensive income

- pro-forma statement of financial position

You must be able to explain why organisations prepare pro-forma statements, their uses and who the users of these statements are. You should also be able to discuss the requirements for preparing pro-forma statements.

You need to be able to prepare a pro-forma statement of comprehensive income using the percent-of-sales method. This is the same method that is used to prepare common-size statements as explained in chapter 3 of the prescribed textbook.

You need to be able to prepare a pro-forma statement of financial position using the judgemental method.

ADDITIONAL SOURCES TO ACCESS

To gain further understanding of cash flow and financial planning, you can access the following sources:

- https://bizfluent.com/info-7742923-budgeting-performance- html, accessed 25 February 2020.

- https://edwardlowe.org/how-to-prepare-a-cash-budget-2/, accessed 25 February

SELF-ASSESSMENT EXERCISES

At the end of this chapter, there is a series of different self-test problems, warm- up exercises, problems and a more comprehensive case study. You should attempt to answer these questions, perform the calculations and use them to practise and re-enforce your learning and understanding. You may submit any of your answers to the lecturer for assessment and feedback.

SBS also shares copies of previous exam papers with you during the semester. The questions in these exam papers are very good examples of what you are expected to know and be able to do having studied and mastered the content of chapter 4 of the prescribed textbook and having followed the guidance provided in this topic.